Czechia (The Czech Republic), similarly to other Eastern European Union countries, struggles with significant losses due to its VAT gap. There are rumours that the Czech Republic will be the first country in the EU to introduce the so-called Generalised Reverse-Charge Mechanism (GRCM). In practice, that would mean the elimination of VAT taxation in the majority of B2B transactions. That would be a revolutionary measure in the fight against VAT fraud. However, there is still no exact date scheduled for when, if at all, GRCM will come into force.

Therefore, the GRCM issue is a question of the future. For now, there are other solutions in place in Czechia (the Czech Republic), which are aimed to make VAT collection more effective. One of the most important is the VAT Control Statement (Kontrolní hlášení DPH) – a detailed transactional VAT reporting requirement. Although the Control Statement is already in force as of 2016, it is worth sharing more details about this obligation, since this is quite complex reporting and businesses may still face issues with Control Statement compliance.

VAT Control Statement – legal background

The VAT Control Statement went into force in January 2016. The legal basis for imposing this requirement is article 101c of the Czech VAT Act. The report needs to be submitted by registered Czech VAT taxpayers, including foreign entities registered for VAT purposes in Czechia (The Czech Republic).

The VAT Control Statement does not substitute the VAT Return and Recapitulative Statement (EC Sales and Purchase List). All those reports need to be submitted to tax authorities in parallel. The deadline for filing the VAT Control Statement is the same as for VAT returns. For taxpayers following the monthly VAT settlement, the submission date is the 25th day after the reporting period.

Not fulfilling VAT Control Statement obligations may be subject to quite serious penalties. The range of sanctions is between CZK 1,000 (EUR 40) to CZK 50,000 (EUR 2,000). In serious cases, when a taxpayer does not file the VAT Control Statement, even after summons from the tax authorities, penalties may be as high as CZK 500,000 (EUR 20,000). Also, similar penalties apply for inaccurate reporting. Worth underlying is the fact that Czech tax authorities are known for their strict approach to data reported in the Control Statement. Even relatively small discrepancies, such as minor differences in values reported in the VAT Return and VAT Control Statements, will be detected by Czech tax authorities and have to be corrected.

VAT Control Statement – scope of reporting

When it comes to the content of the reporting, the Czech VAT Control Statement is quite similar to the Polish JPK_VAT or Slovakian obligation (also known as Control Statement), for example. What has to be reported are details about taxpayer transactions performed, including for example customer VAT IDs or the date of supply (the so-called DUZP – Datum uskutečnění zdanitelného plnění), which are not always easy to determine.

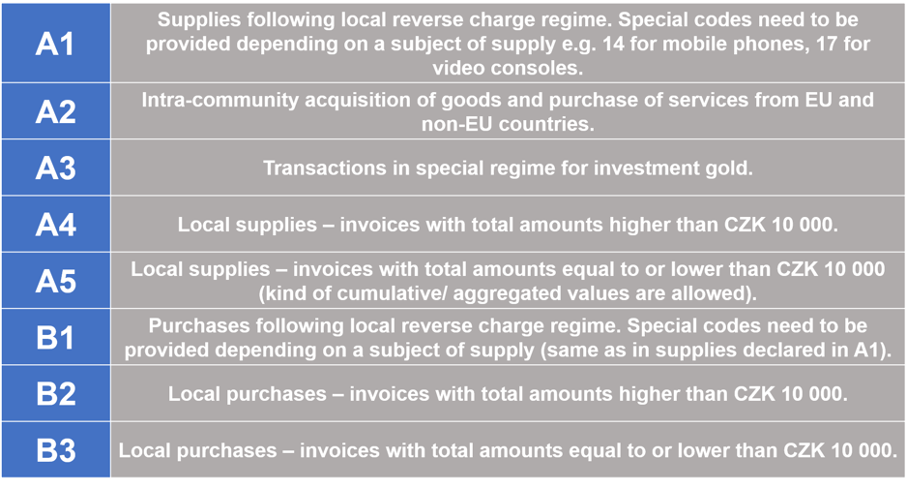

The VAT Control Statement has a specific layout and is divided into eight sections, in which data about transactions need to be reported: A1 to A5, and B1 to B3.

Apart from the above sections, there is a separate area (section C) in which total values reported in A1-A5 and B1-B3 are calculated. Also, corresponding fields (so called boxes) in the VAT return are indicated. For example, A1 values need to be equal to Box 25 in the VAT return.

VAT Control Statement – technical outline

The required format of reporting is an XML file. The scheme (XSD structure) of the XML file is labelled as DPHK1 and might be found in Daňový portal, through which electronic tax reporting is performed.

The generated XML file may be uploaded to the aforementioned portal. Before submission, a taxpayer has the possibility to verify uploaded values and make any required amendments. The portal allows for submission of other VAT reports, such as the VAT Return (DPHDP3) or Recapitulative Statement (DPHSHV).

Considering the complexity of the VAT Control Statement report and strict approach of the Czech tax authorities, it is advisable to ensure correct reporting, both from a technical and a VAT regulation perspective. “Work around” solutions relying on, for example, spreadsheets are quite sensitive to differences in data formatting, or human-error. In order to avoid such “surprises” automated generation from the ERP system (for example SAP solution) might be considered.

Our company, SNI, provides SAP solution for Control Statements, as well as, other Czech VAT reports, including the VAT Return and Recapitulative Statement.